The follwing report was written by The Federal Reserve itself. The related links follow at the end of the piece. I thought the stock market was rigged before...I had no idea.

Federal Reserve Bank of New York

July 11, 2012

The Puzzling Pre-FOMC Announcement “Drift”

We show that since 1994, more than 80 percent of the equity premium on U.S. stocks has been earned over the twenty-four hours preceding scheduled Federal Open Market Committee (FOMC) announcements (which occur only eight times a year)—a phenomenon we call the pre-FOMC announcement “drift.”

The Drift: A First Take

The pre-FOMC announcement drift is best summarized in the chart below, which provides two main takeaways:

- Since 1994, there has been a large and statistically significant excess return on equities on days of scheduled FOMC announcements.

- This return is earned ahead of the announcement, so it is not related to the immediate realization of monetary policy actions. (Unless, of course, someone knows what the announcement will be. This is also known as "frontrunning", "smart money" and "insider trading")

The solid black line displays the average cumulative return starting at the market’s opening on the day before each scheduled FOMC announcement to the market’s close on the day after each announcement. Our sample period starts in 1994, when the Federal Reserve began announcing its target for the federal funds rate regularly at around 2:15 p.m. Following the announcement, equity prices may fluctuate widely, but on balance, they end the day at about their 2 p.m. level, 50 basis points higher than when the market opened on the day before the FOMC announcement. Since 1994, returns are essentially flat if the three-day windows around scheduled FOMC announcement days are excluded. In a nutshell, the figure shows that in the sample period the bulk of the rise in U.S. stock prices has been earned in the twenty-four hours preceding scheduled U.S. monetary policy announcements.

|

| Yes, the SP-500 would be about 600 (it's at 1370 now) without these "mysterious" returns. |

Surprisingly, though, we don’t find any differential returns for these assets on FOMC days compared with other days. In other words, the pre-FOMC drift is restricted to equities Further, we don’t find analogous drifts ahead of other macroeconomic news releases, such as the employment report, GDP and initial claims, among many others. The effect is therefore restricted to FOMC, rather than other macroeconomic, announcements. (This is a global banking cartel, not just the U.S. The FOMC is the "Godfather" )

The authors conclude with the following statement:

The authors conclude with the following statement:Our findings suggest that the pre-FOMC announcement drift may be key to understanding the equity premium puzzle since 1994. However, at this point, the drift remains a puzzle.

Maybe this article can help solve the ENIGMA...

By Michael Kitchen, MarketWatch

LOS ANGELES (MarketWatch) — The Bank of Japan stepped back into the stock market Monday, making its largest single-day purchase of exchange-traded funds to date. The Japanese central bank said it spent 39.7 billion yen (about $500 million) buying up stock ETFs as part of its ongoing asset-purchase program. Since the 2008 collapse of Lehman Brothers and ensuing global crisis, central banks around the world have embarked on a spree of asset-buying meant to avoid deflation and, to a certain extent, support the markets. The Bank of Japan has bought almost ¥1 trillion worth of ETFs — along with another ¥78.9 billion in REITs — and has an additional ¥642 billion to spend on the stock funds after raising the program’s size at it last policy meeting in April.

The central bank emphasizes that the program has only broad goals such as supporting interest rates and reducing risk premiums, rather than supporting financial markets (if you're gonna lie, lie large)

Naomi Fink Jefferies Japan’s head of Japanese strategy says that while the ETF purchases are really part of the broad push to reflate asset prices in the deflation-plagued country, they do “provide a bit of a backstop, when they think they can curb the downside” for the market. (this was called the "Greenspan put" in the U.S, now replaced by the "Bernake guarantee")

“Still, it’s a very small amount,” Fink said of the ETF purchases. ($500 million is chump-change when you can print it yourself) “It’s more designed to bolster sentiment ... [and] it works best when sentiment is fragile.” (i.e. the markets are falling)

LOS ANGELES (MarketWatch) — The Bank of Japan stepped back into the stock market Monday, making its largest single-day purchase of exchange-traded funds to date. The Japanese central bank said it spent 39.7 billion yen (about $500 million) buying up stock ETFs as part of its ongoing asset-purchase program. Since the 2008 collapse of Lehman Brothers and ensuing global crisis, central banks around the world have embarked on a spree of asset-buying meant to avoid deflation and, to a certain extent, support the markets. The Bank of Japan has bought almost ¥1 trillion worth of ETFs — along with another ¥78.9 billion in REITs — and has an additional ¥642 billion to spend on the stock funds after raising the program’s size at it last policy meeting in April.

The central bank emphasizes that the program has only broad goals such as supporting interest rates and reducing risk premiums, rather than supporting financial markets (if you're gonna lie, lie large)

Naomi Fink Jefferies Japan’s head of Japanese strategy says that while the ETF purchases are really part of the broad push to reflate asset prices in the deflation-plagued country, they do “provide a bit of a backstop, when they think they can curb the downside” for the market. (this was called the "Greenspan put" in the U.S, now replaced by the "Bernake guarantee")

“Still, it’s a very small amount,” Fink said of the ETF purchases. ($500 million is chump-change when you can print it yourself) “It’s more designed to bolster sentiment ... [and] it works best when sentiment is fragile.” (i.e. the markets are falling)

Hmmm. Fragile you say? I'm sure our Federal Reserve doesn't do this because this is America and we believe in life, liberty, fair play and equal opportunity! Accept the consequences of your actions! Sleep in the bed you made!...oh...wait a minute here....

|

| From lower left to upper right, FED open market actions of 1% interest rates, QE1, QE2, Operation Twist 1, Operation Twist 2. |

You are witnessing the "QE" bubble, where the FED itself, in concert with other Central Banks, is forcing the market higher. Actually printing money with QE and actually buying stocks at critical market junctures. I'm sure this will end well. It did for Zimbabwe.

This piece describes what all the Central Banks have been up to..

By James Bianco - January 27th, 2012

The combined size of these eight central banks’ balance sheets has almost tripled in the last six years from $5.42 trillion to more than $15 trillion and is still on the rise!

Prior to the 2008 financial crisis, the eight central bank balance sheets were less than 15% the size of world stock markets and falling. In the immediate aftermath of Lehman Brothers’ failure, these eight central bank balance sheets swelled to 37% the capitalization of the world stock market. Recently, the eight central bank balance sheets have spiked back to 33% of world stock market capitalization. This has come about not by lender of last resort loans, but rather by QE expansion (buying bonds with “printed money“) even faster than world stock markets are rising. Central banks are ruling markets to a degree this generation has not seen. Collectively they are printing money to a degree never seen in human history.

Prior to the 2008 financial crisis, the eight central bank balance sheets were less than 15% the size of world stock markets and falling. In the immediate aftermath of Lehman Brothers’ failure, these eight central bank balance sheets swelled to 37% the capitalization of the world stock market. Recently, the eight central bank balance sheets have spiked back to 33% of world stock market capitalization. This has come about not by lender of last resort loans, but rather by QE expansion (buying bonds with “printed money“) even faster than world stock markets are rising. Central banks are ruling markets to a degree this generation has not seen. Collectively they are printing money to a degree never seen in human history.

Until a worldwide exit strategy can be articulated and understood, risk markets will rise and fall based on the perceptions and realities of central bank balance sheets. As long as this is perceived to be a good thing, like perpetually rising home prices were perceived to be a good thing, risk markets will rise.

|

| Here's how the housing bubble turned out |

When/If these central banks go too far, as was eventually the case with home prices, expanding balance sheets will no longer be looked upon in a positive light. Instead they will be viewed in the same light as CDOs backed by sub-prime mortgages were when home prices were falling. The heads of these central banks will no longer be put on a pedestal but looked upon as eight Alan Greenspans that caused a financial crisis.

The tipping point between balance sheet expansion being bullish for risk assets versus bearish is impossible to know. Given the growth rate of central bank balance sheets around the world over the past few years, we might not have to wait too long to find out. Enjoy it while it's still bullish.On Bianco's "tipping point", I believe "difficult" is a better term than "impossible". Here's why: (click to enlarge)

|

| Stocks are becoming less responsive with each intervention. As with a drug addict, each dose has to be a little stronger to get the same high as before. |

Two distinct peaks form, and the double top confirms (a valid pattern) when price pierces the lowest low between the peaks (2002-2003) which it did in 2009. Normally, this would indicate a downtrend (lower prices ahead) in an individual stock. This isn't an individual stock though, this is 500 of the strongest companies in the world, and the bellweather for the U.S., and world, economy.

This chart highlights (apologies for the tech-talk) a large, negative divergence in the oscillator, the blue bottom half. As stocks were rising in the second housing peak, the oscillator was falling. A lot. Think of it as a crowd "running with the bulls". The first crowd in the dot-com top was much larger than the housing top crowd. This indicates a high probability the second top (housing) will not significantly surpass the previous peak, as there are a lot more people waiting to sell at that price than there are wanting to buy. Stocks hit a brick wall at the 1570 level and subsuquently lost over half their value. Notice also the 3rd, QE-induced peak is the smallest of all. If price gets near the Dot-com / housing level (1550-1570 on the sp-500) this tells us it's likely to fail there.

This chart highlights (apologies for the tech-talk) a large, negative divergence in the oscillator, the blue bottom half. As stocks were rising in the second housing peak, the oscillator was falling. A lot. Think of it as a crowd "running with the bulls". The first crowd in the dot-com top was much larger than the housing top crowd. This indicates a high probability the second top (housing) will not significantly surpass the previous peak, as there are a lot more people waiting to sell at that price than there are wanting to buy. Stocks hit a brick wall at the 1570 level and subsuquently lost over half their value. Notice also the 3rd, QE-induced peak is the smallest of all. If price gets near the Dot-com / housing level (1550-1570 on the sp-500) this tells us it's likely to fail there. Barry Ritholtz, a money manager for high net-worth indiduals and financial blogger, had this to say recently:

"What makes this environment so challenging is that without the certainty of another round of QE investors are more likely to be risk off (pull money out of stocks). What's preventing this from becoming a rout (market crashing or correcting) — is the fear of getting caught under-invested or (heaven forbid short) when the next Ben Bernanke helicopter drop(Quantitative Easing, printing money) flies into town . . ."

And there you have it. Earnings? nah. Sales? nah. Jobs? nah. The only thing that now matters to "investors" of every stripe is how much money is going to be created, and when.

Notice Barry also says "heaven forbid short" as well. This warrants an explanation so bear with me. In Stocks, a "bearish" bet is for lower prices ahead (short) and a "bullish" bet is for higher prices (long). "Shorting" means betting the market will fall, profiting when it does, and potentially losing more than you have if the market rises instead. While vilified in the media as evil and causing stocks to go down (which is false), short sellers serve a very important function: When they close their short position, they have to actually buy the stock they were shorting, at it's current price. This is called "covering". Thus, short covering is the same as buying long, and this adds fuel to market rallies. Short Covering and Long Buying combine to form powerful, lasting rallies. In their quest for a "can't lose" market to maintain the illusion of health, the FED has stopped all major declines since 2008.

|

| "Helicopter" Ben Bernake |

Notice Barry also says "heaven forbid short" as well. This warrants an explanation so bear with me. In Stocks, a "bearish" bet is for lower prices ahead (short) and a "bullish" bet is for higher prices (long). "Shorting" means betting the market will fall, profiting when it does, and potentially losing more than you have if the market rises instead. While vilified in the media as evil and causing stocks to go down (which is false), short sellers serve a very important function: When they close their short position, they have to actually buy the stock they were shorting, at it's current price. This is called "covering". Thus, short covering is the same as buying long, and this adds fuel to market rallies. Short Covering and Long Buying combine to form powerful, lasting rallies. In their quest for a "can't lose" market to maintain the illusion of health, the FED has stopped all major declines since 2008.

|

| Volume is diminishing on each subsequent intervention |

|

| Short Interest, 2006-2012 Hasta la Vista...Shorts. |

This lack of short-covering "fuel" shows in the declining trading volumes and increasingly ineffective interventions.

Before this Fed-induced unshortable market, short-covering served to stop violent, one-way market declines. As the market fell by large percentages, the shorts were the ONLY ones "buying", since they have to cover their position (buy) to make any money. These "short-covering" rallies interrupted violent declines, gave "bulls" a chance to jump in, and allowed opportunities for the market to stabalize or reverse itself. Now that the Fed has made it "safe", the shorts are disappearing, while the longs are sitting on their wallets waiting for the Fed to "guarantee" them a risk-free market. When the market starts a serious decline now, it's natural defense (short covering) has been drugged out of the system by Dr. Bernake. The declines will be swift, and wholly dependent on money printing, or rumors of money printing, to stop them. Bernake and the Fed have removed the fire-breaks in the forest, leaving his "liquidity helicopter" as the only mechanism to fight the inevitable fire.

Before this Fed-induced unshortable market, short-covering served to stop violent, one-way market declines. As the market fell by large percentages, the shorts were the ONLY ones "buying", since they have to cover their position (buy) to make any money. These "short-covering" rallies interrupted violent declines, gave "bulls" a chance to jump in, and allowed opportunities for the market to stabalize or reverse itself. Now that the Fed has made it "safe", the shorts are disappearing, while the longs are sitting on their wallets waiting for the Fed to "guarantee" them a risk-free market. When the market starts a serious decline now, it's natural defense (short covering) has been drugged out of the system by Dr. Bernake. The declines will be swift, and wholly dependent on money printing, or rumors of money printing, to stop them. Bernake and the Fed have removed the fire-breaks in the forest, leaving his "liquidity helicopter" as the only mechanism to fight the inevitable fire. In summary:

You have two distinct tops in the SP-500 since 2000. A third peak is forming now. Below I describe each chart event in more detail. We'll call them...the 3 Tops.

|

| The 3 Tops |

Since 1994: 80% of all stock market returns earned in the 24 hours preceding FOMC announcements. This marks the beginning of the "Easy Money" era for Wall Street.

TOP 1

SP-500 High 1552 March 2000

SP-500 High 1552 March 2000

The 2000 Dot-com top was based on massive corporate accounting fraud that led to rampant speculation. Once everyone realized these prices were based on fruad, the bubble popped and the market corrected. Some executives went to jail, some accounting firms (Arthur Anderson) went bust or to jail, and the market corrected until the Fed intervened in 2003.

Urban Legend de-bunked: Stocks always go up.

2003 FED arrests the falling markets by slashing it's Fed funds rate (the price big banks get money for) to 1%

|

| Fed funds rate v. SP-500 Housing Peaked in 2006...EXACTLY when banks had to start paying over 5% for their money. The market partied on for a few months, then tanked. |

Fresh off the Fed saving the day with 1% rates, the Too Big To Fail Banks, fueled by easy money from the Fed, create the housing bubble through mortgage securitization.

TOP 2

SP-500 High 1576 October, 2007

Credit, lending and mortgage fraud are rampant, and a few months after the Fed raises rates to 5% the market implodes. Credit Fraud Top 2 cannot withstand reality any better than Accounting Fraud Top 1 did. Massive loan losses were put on the taxpayers while Wall Street paid record bonuses. Zero arrests were made. Every problem that existed in 2009 is not only unresolved they are larger. The Too Big Too Fail Banks are now 25% bigger and backstopped by the government. This time, the correction is faster and deeper though, and ushers in what will be the last bubble...Central Bank Money Printing. The QE bubble.

SP-500 High 1576 October, 2007

Credit, lending and mortgage fraud are rampant, and a few months after the Fed raises rates to 5% the market implodes. Credit Fraud Top 2 cannot withstand reality any better than Accounting Fraud Top 1 did. Massive loan losses were put on the taxpayers while Wall Street paid record bonuses. Zero arrests were made. Every problem that existed in 2009 is not only unresolved they are larger. The Too Big Too Fail Banks are now 25% bigger and backstopped by the government. This time, the correction is faster and deeper though, and ushers in what will be the last bubble...Central Bank Money Printing. The QE bubble.

Urban Legend de-bunked: Home prices always go up.

Urban Legend de-bunked: Home prices always go up.

March, 2009 Fed launches QE1, unleashing $1.2 Trillion in freshly printed cash on equity markets.

August, 2010, Fed announces QE2, unleashing $600 billion in freshly printed cash on equity markets in September 2010.

September, 2011 Fed announces Operation Twist, where they don't print money but they manipulate mortgage rates.

June 2012 Fed announces Operation Twist 2, but still aren't printing money. The market has barely achieved the highs reached from QE2.

TOP 3

SP-500 High ???? When ????

SP-500 High ???? When ????

|

Future QE peak (based on manipulating markets with printed money). In an effort to protect the status quo, prevent losses to bond holders, and maintain the illusion of prosperity, Central Banks have printed over $15 Trillion in 4 years, often injecting that directly into equity markets. Most people are unaware of just how much a Trillion is. Allow me to illustrate. Picture a stack of $100 bills. To most people, $100 is not a bill you'd want to fall out of your wallet.

A US dollar bill is .0043 inches thick. Assuming the same for a 100 dollar bill, a stack of 100 dollar bills totalling one million dollars would be 43 inches tall.

It takes 10,000 such bills to equal a million dollars. 10,000 X .0043 = 43 inches.

Using these measurements, a billion dollars would be just over 3583 feet tall, and a trillion dollars would be just over 678.66 miles tall!

Multiply 678.66 by the $15 Trillion Central Banks have printed since 2008 = A stack of $100 bills 10,180 miles high.

A US dollar bill is .0043 inches thick. Assuming the same for a 100 dollar bill, a stack of 100 dollar bills totalling one million dollars would be 43 inches tall.

It takes 10,000 such bills to equal a million dollars. 10,000 X .0043 = 43 inches.

Using these measurements, a billion dollars would be just over 3583 feet tall, and a trillion dollars would be just over 678.66 miles tall!

Multiply 678.66 by the $15 Trillion Central Banks have printed since 2008 = A stack of $100 bills 10,180 miles high.

The Gump analogy

|

| Savannah to L.A. |

to Los Angeles, coast to coast. Assume our stack of 100's can't fall over water so it doubles back every time it hits the coast. You run back and forth until you find the top of that money stack.

|

| L.A. to Savannah |

|

| Savannah to L.A. |

|

L.A. to Savannah |

You run coast to coast 4 times, along your fallen stack of $100 bills, and you are STILL about 500 miles short of the top. At this point, you're tired of being a millionaire every time you run two steps. You just want to go home, find Jen-ney, and get Loo-ten-nant Dan to manage your portfolio.

How high can the SP-500 go when the third and final top, built on printing money out of thin air, inevitably ends? Theoretically, since Central Banks can print infinite amounts of money and are buying stocks, the market should always rise. Sellers will be overwhelmed by buyers who never run out of money.

|

| "15 Trillion is a whole LOT of Mon-ney." |

Will it surpass 1552, the Dot-Com peak based on Accounting Fraud? Or 1576, the Housing peak based on credit fraud? At least those bubbles had some effect on Main Street, although whatever money Mainstreet made in stocks or housing was usually taken back with interest when the bubble popped.

This current bubble, however, is exclusively for those with income streams tied directly to Washington or Wall Street, and is the most artificial of the three.

Top 1: Artificially high Stocks via Accounting Fraud.

Top 2: Artificially high Home Prices via Credit Fraud.

Top 3: Artificially high Equity Markets via Monetary Fraud.

|

| 3 Tops. The Law Firm of Fraud, Fraud and Print'em. |

|

| How "Too Big to Fail" banks "launder" their profits. |

Urban Legends about to be de-bunked: The cure for too much bad debt is more debt / reality doesn't matter /we can print our way to prosperity / we can control markets forever.

The real economy has been deteriorating under the weight of too much debt, not enough good jobs, accounting fraud, credit fraud and now monetary fraud since 2000, as evidenced here.

|

| U.S. Population v. Jobs 8% unemployment my ass. |

|

| Feed the hungry so they don't riot in the streets |

|

| Consumer Prices v. Civilian Employment On Main Street jobs are vanishing AND everything is getting more expensive because of all the money-printing. |

|

| Employed or looking for work, 1984-2012. Peaked in...wait for it...2000. Now at 30 year low.  |

|

| We're in for some weather... |

The only way we can begin to resolve the structural imbalances that are spiraling out of control in our economy is to allow free markets and capitalism (not cronyism) to return. Let the market fall. Stop intervening. Send banksters to jail. Let failed banks fail. Prosecute fraud. Enforce the law, equally and consistently. Crime can't pay more than honest jobs, but in this day and age it damn sure does. This must change. Let what has to happen happen, clean up the mess and build anew. A generation of Americans learned some very tough lessons during the Great Depression that led to the most prosperous 50 years in human history.

"You cannot escape the responsibility of tommorrow by evading it today" -Abraham Lincoln

Unfortunately, our leaders have forgotten the lessons of the Great Depression and the wisdom of Abraham Lincoln. Which will make the inevitable lessons that much harsher when they arrive.

|

| Total Credit Market Debt v. Money Supply "If we print fast enough, maybe no one will notice nobody's paying back these loans!" If loans were being repaid through organic growth, these lines would intersect... |

|

| Incomes, paid for with debt. Living the dream. |

|

| 50-month moving average about to cross under the 200 month. A "Death Cross" signal. |

This signal is bearish in stocks when using daily or weekly charts. On the monthly scale, it's like one of these moving into our solar system.

This signal is bearish in stocks when using daily or weekly charts. On the monthly scale, it's like one of these moving into our solar system.Note the deterioration of the MACD at all 3 peaks as price was still rising. This is a "non-confirmation" (lower highs while the market is making higher highs)

|

| Here I've highligted the reverse..MACD "confirmation". Lower lows to match the market's lower lows |

"Mischief springs from the power which the moneyed interest derives from a paper currency which they are able to control, from the multitude of corporations with exclusive privileges... which are employed altogether for their benefit"

-Andrew Jackson

|

| We are running out of road to kick the can down. |

|

| Fraud, Fraud, and Legal Counterfeiting. Reality seems to assert itself at the 1500-1600 level. |

Charles Ponzi would be so proud...

|

| I wasn't a crook! I was just a Central Banker ahead of my time! |

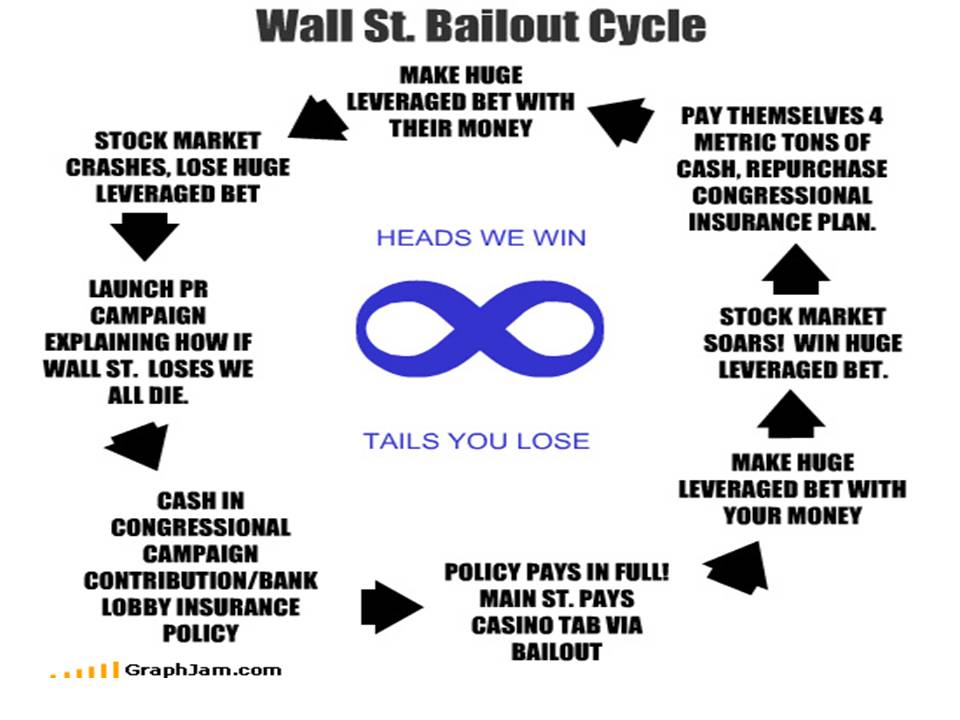

The way stocks used to work

NEW YORK FED: http://libertystreeteconomics.newyorkfed.org/2012/07/the-puzzling-pre-fomc-announcement-drift.html

balance sheet

http://www.ritholtz.com/blog/2012/01/living-in-a-qe-world/

http://www.ft.com/intl/cms/s/0/78953f1e-87a2-11e1-ade2-00144feab49a.html#axzz1sPGv51ig

http://www.marketwatch.com/story/bank-of-japan-buys-record-amount-of-stock-etfs-2012-05-07

http://www.zerohedge.com/news/bank-japan-goes-full-tilt-buys-record-amount-etfs-and-reits-open-market-prevent-market-collapse?utm_source=feedburner&utm_medium=feed&utm_campaign=Feed%3A+zerohedge%2Ffeed+%28zero+hedge+-+on+a+long+enough+timeline%2C+the+survival+rate+for+everyone+drops+to+zero%29

http://www.zerohedge.com/news/chart-year-fed-has-doubled-sp-admits-fed?utm_source=feedburner&utm_medium=feed&utm_campaign=Feed%3A+zerohedge%2Ffeed+%28zero+hedge+-+on+a+long+enough+timeline%2C+the+survival+rate+for+everyone+drops+to+zero%29

No comments:

Post a Comment